New Zealand's national dataset

The National Infrastructure Pipeline (Pipeline) is New Zealand's national dataset of infrastructure initiatives, recording activity at various stages of planning, funding commitment, and delivery across central government, local government, and private sector infrastructure providers. Updated quarterly, it serves as an important evidence base informing investment decisions to maintain, renew, and improve New Zealand's infrastructure.

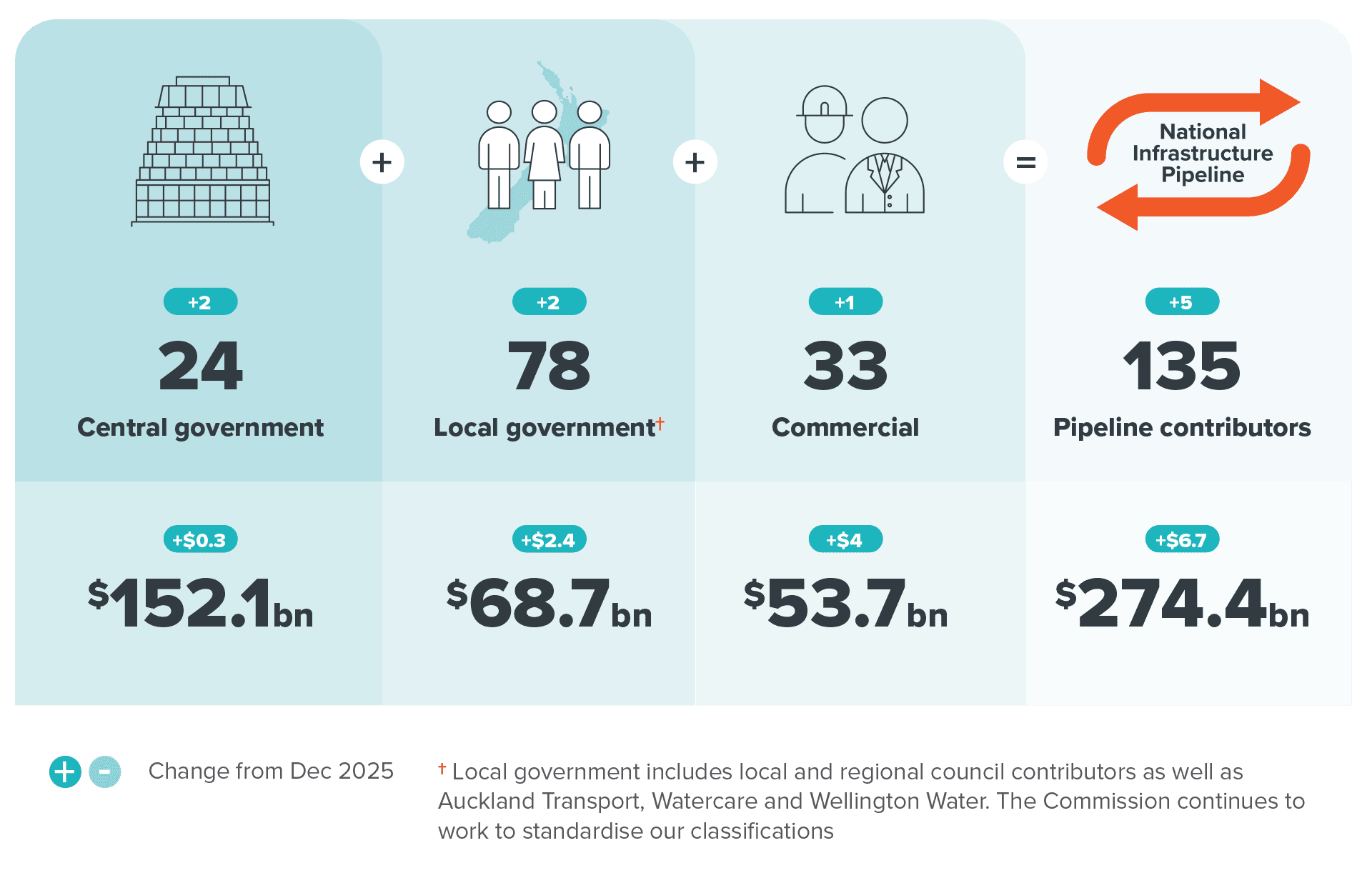

With 135 infrastructure providers contributing information, the Pipeline is building towards a complete system-wide view of activity. Airports, electricity networks, ports, water sector providers, and other commercial infrastructure providers yet to contribute information should reach out to the Commission to participate and profile their projects in the Pipeline.

More initiatives secure funding and progress into delivery

The March Pipeline update shows that between December 2025 and March 2026:

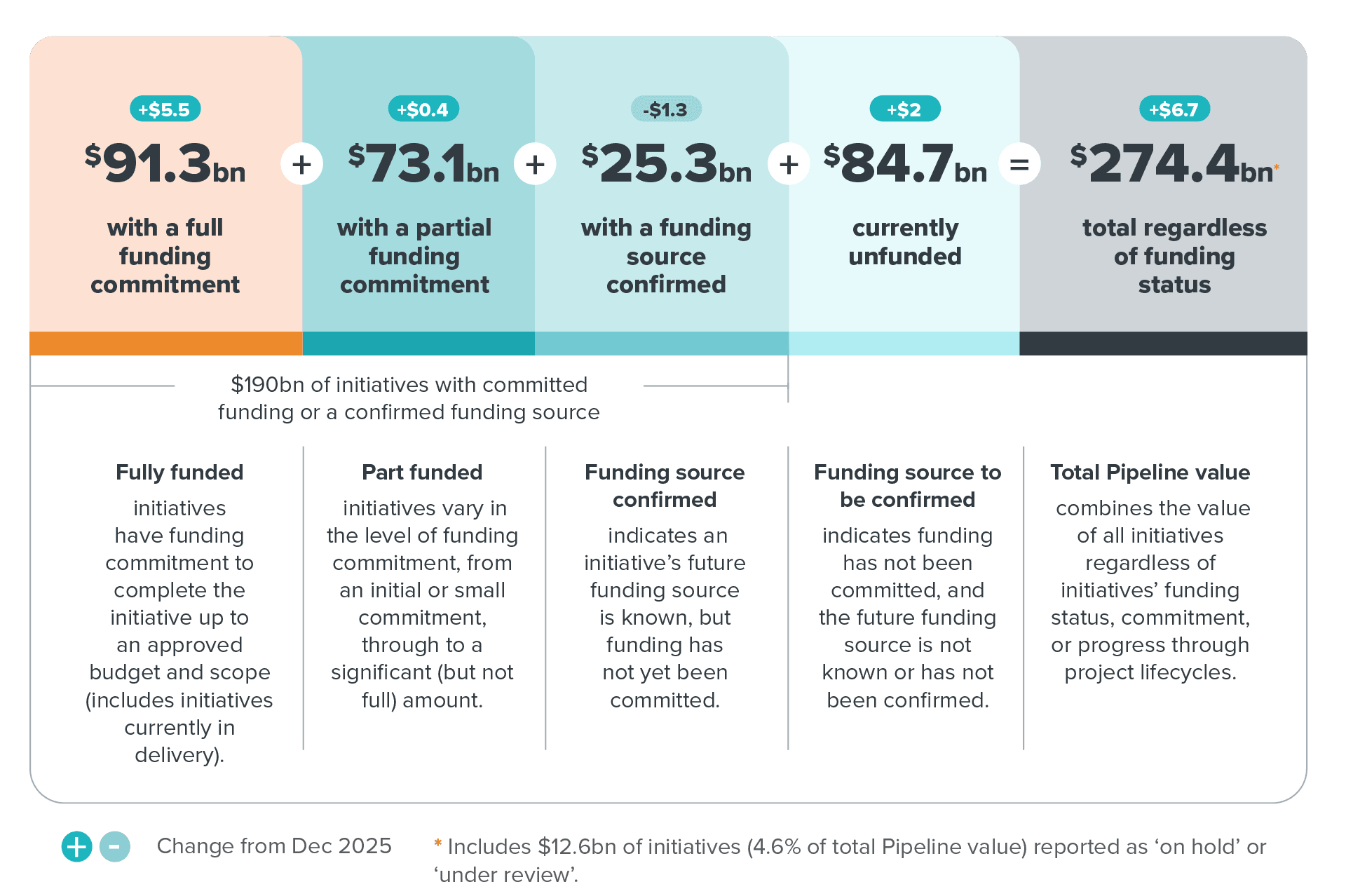

- Fully funded initiatives increased by $5.5 billion to $91 billion – including $4 billion from initiatives progressing from an earlier funding status to full funding commitment.

- The combined value of initiatives with committed funding or a confirmed funding source increased by $4.7 billion to $190 billion – reflecting continued progression of initiatives through planning.

- Total Pipeline value increased by $6.7 billion to $274 billion – driven primarily by the addition of new initiatives and adjustments to expected costs of existing initiatives, including those in planning and construction.

- Initiatives under construction increased by $2.8 billion to $71 billion – illustrating the total value of work currently being delivered.

This Pipeline snapshot reflects data available as at the end of March 2026. Some central government infrastructure projects listed as unfunded may receive funding commitments through Budget 2026. June quarter Pipeline data will reflect changes in funding status as a result of Budget decisions.

Download this snapshot

Pipeline Snapshot - March 2026

Download

The Pipeline at a glance

In March 2026 the Pipeline included information on almost 12,500 1 infrastructure initiatives. These initiatives span projects and programmes at various states of funding commitment.

Pipeline value by funding status

Alongside funding status, the Pipeline can be disaggregated by lifecycle stage, tracing the progression of initiatives from planning to construction and providing forward visibility of work entering the market.

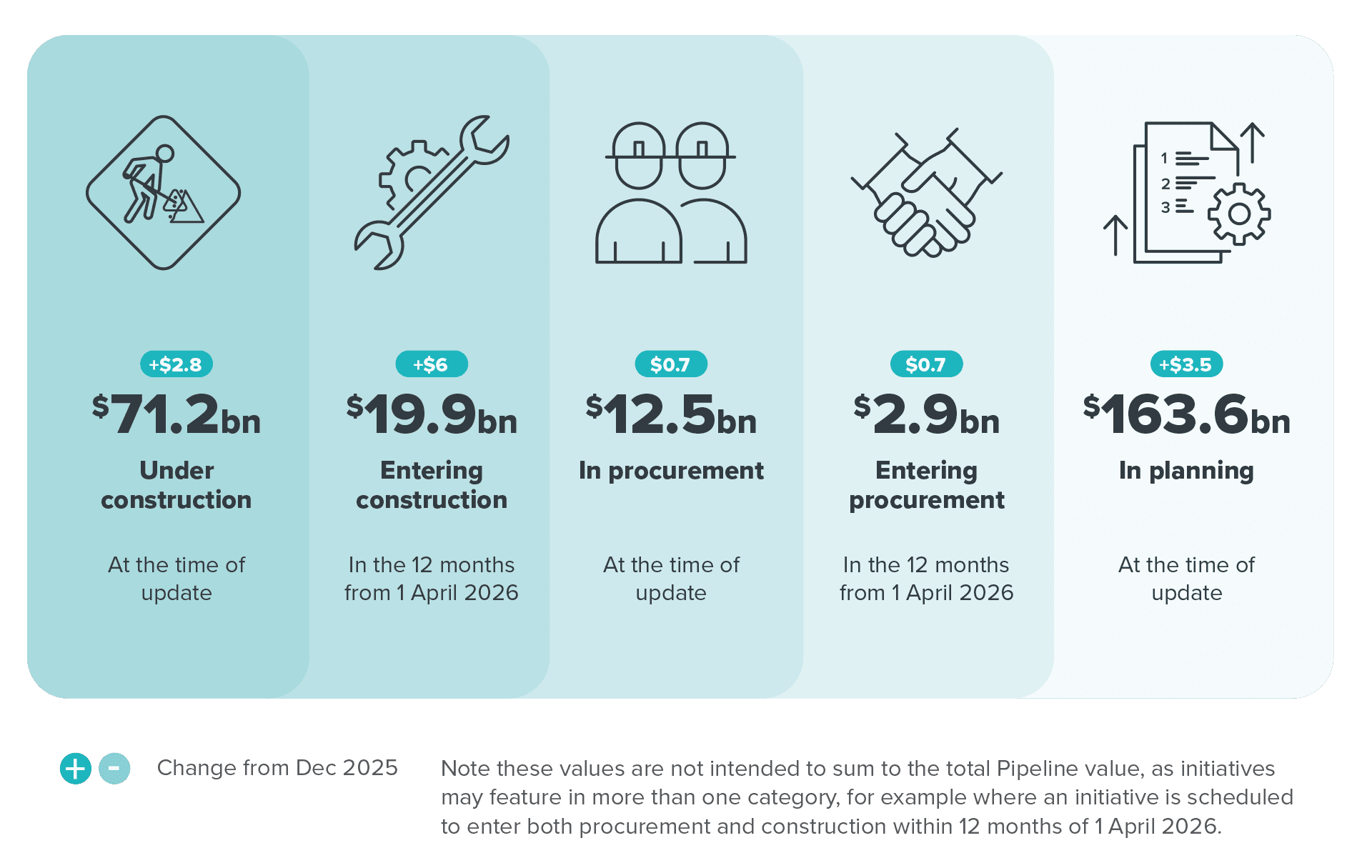

Pipeline value by initiatives' progression through the project lifecycle

Initiatives entering procurement

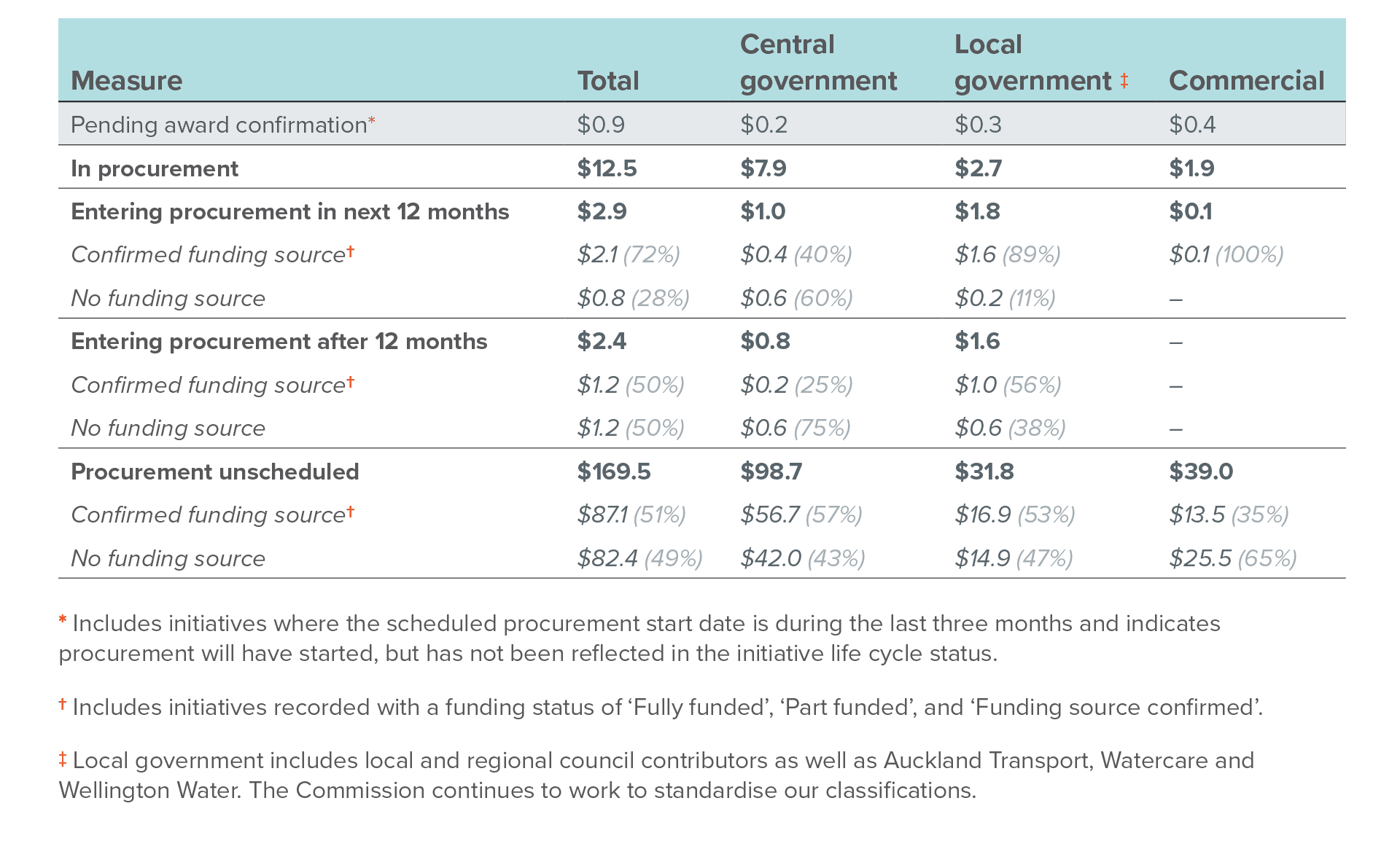

In March, $12.5 billion of initiatives were progressing through procurement processes, up from $11.8 billion in the previous quarter. Central government infrastructure providers accounted for 63% of this activity. Many providers are reluctant to signal procurement timelines until initiatives are sufficiently advanced. This means the $2.9 billion of procurement activity currently indicated for the next 12 months likely understates forward activity. Budget 2026, scheduled for 28 May, has the potential to give some infrastructure providers greater certainty.

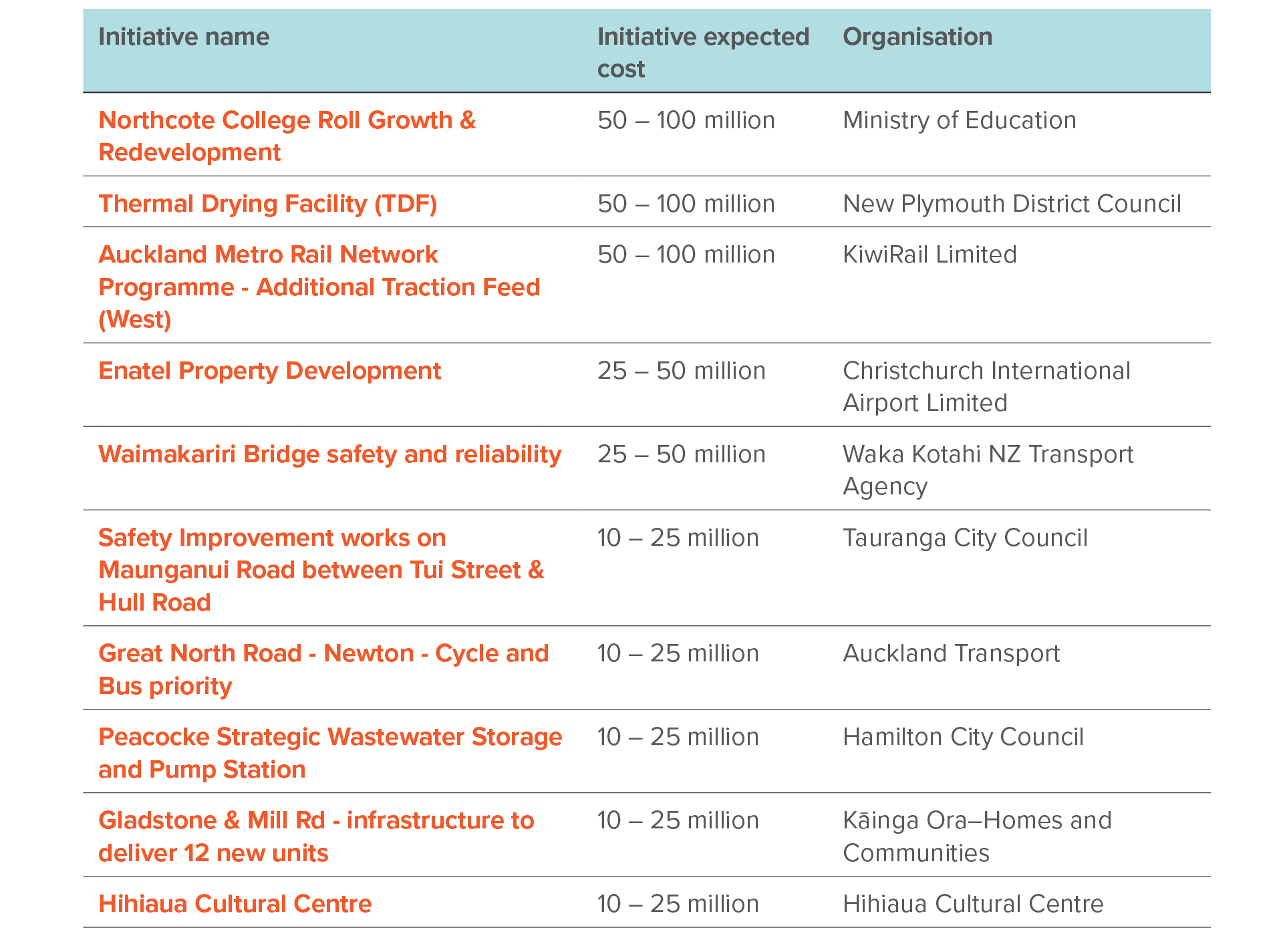

There are 7309 initiatives in various stages of planning in the Pipeline. Table 1 shows the total expected cost of these initiatives by procurement timing across central government, local government, and commercial infrastructure providers. The italicised text provides additional context on the level of commitment for these initiatives.

Table 1: Breakdown of Pipeline value scheduled to enter procurement, 1 April 2026 – 31 March 2027

All values are recorded in $ billions.

Initiatives entering construction

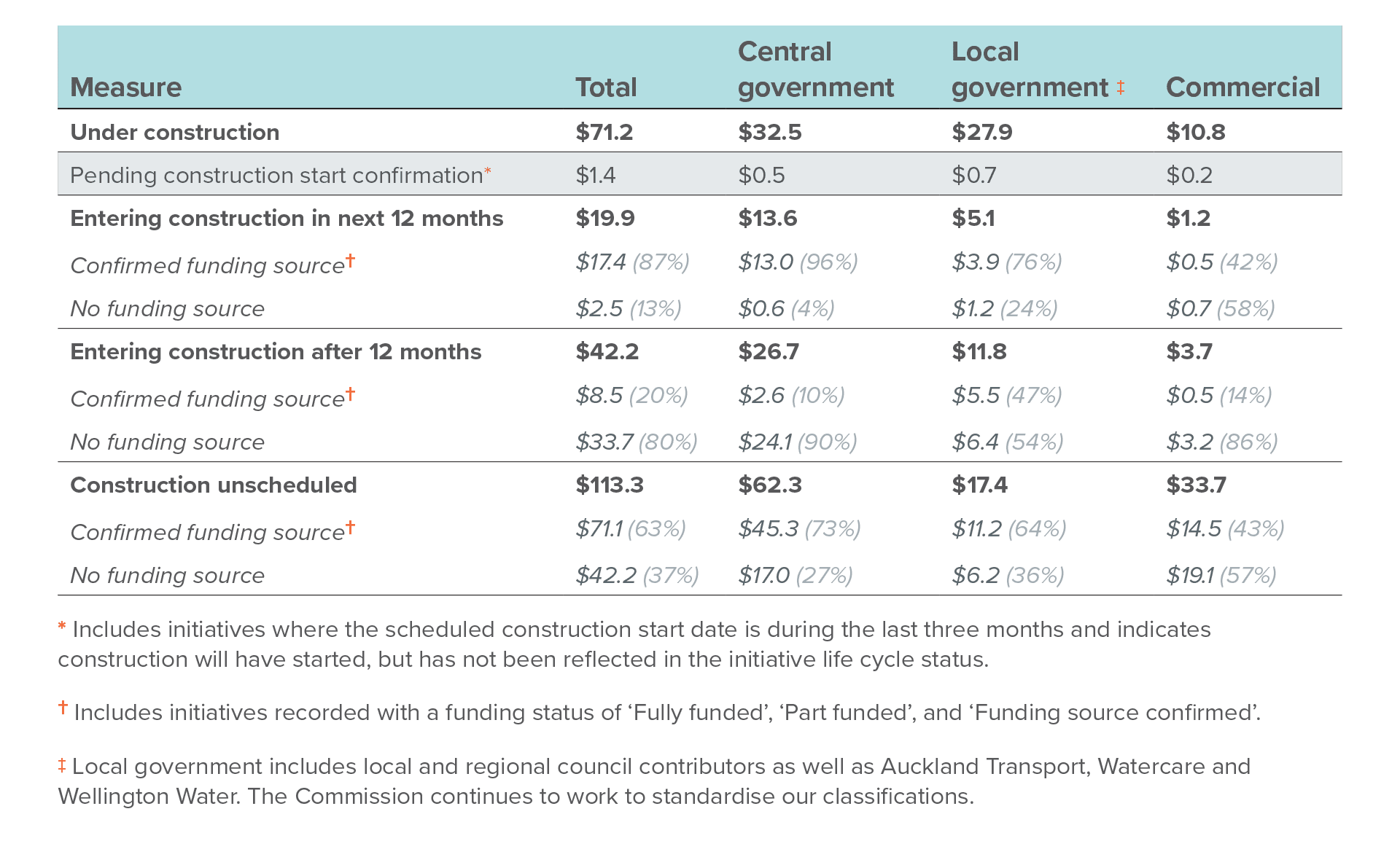

Over 3,000 initiatives with a total expected cost of $71.2 billion were reported as under construction. Delivery of these initiatives is projected to result in $3.8 billion of spend in the April to June 2026 quarter, with a further $5.9 billion currently projected for the period, July to December 2026.

Table 2 shows the total expected cost for initiatives in the Pipeline that were under construction at the time of the update, and the value of initiatives that are expected to enter construction. The rows highlight the progression of initiatives across the planning horizon, including highlighting increasing funding commitments for near-term activity. The certainty of construction-start dates also improves as initiatives advance, funding is committed, and contracts are awarded.

Pipeline contributors’ March updates indicate around $20 billion of initiatives are expected to enter construction in the next 12 months, with 87% reported as fully funded, part funded, or with a confirmed funding source.

Table 2: Breakdown of Pipeline value scheduled to enter construction, 1 April 2026 – 31 March 2027

All values are recorded in $ billions.

The change in Pipeline value between December 2025 and March 2026 is discussed later in this report.

Pipeline composition and funding commitment

Scale of initiatives in the Pipeline

Smaller initiatives support a steady flow of work for the construction sector

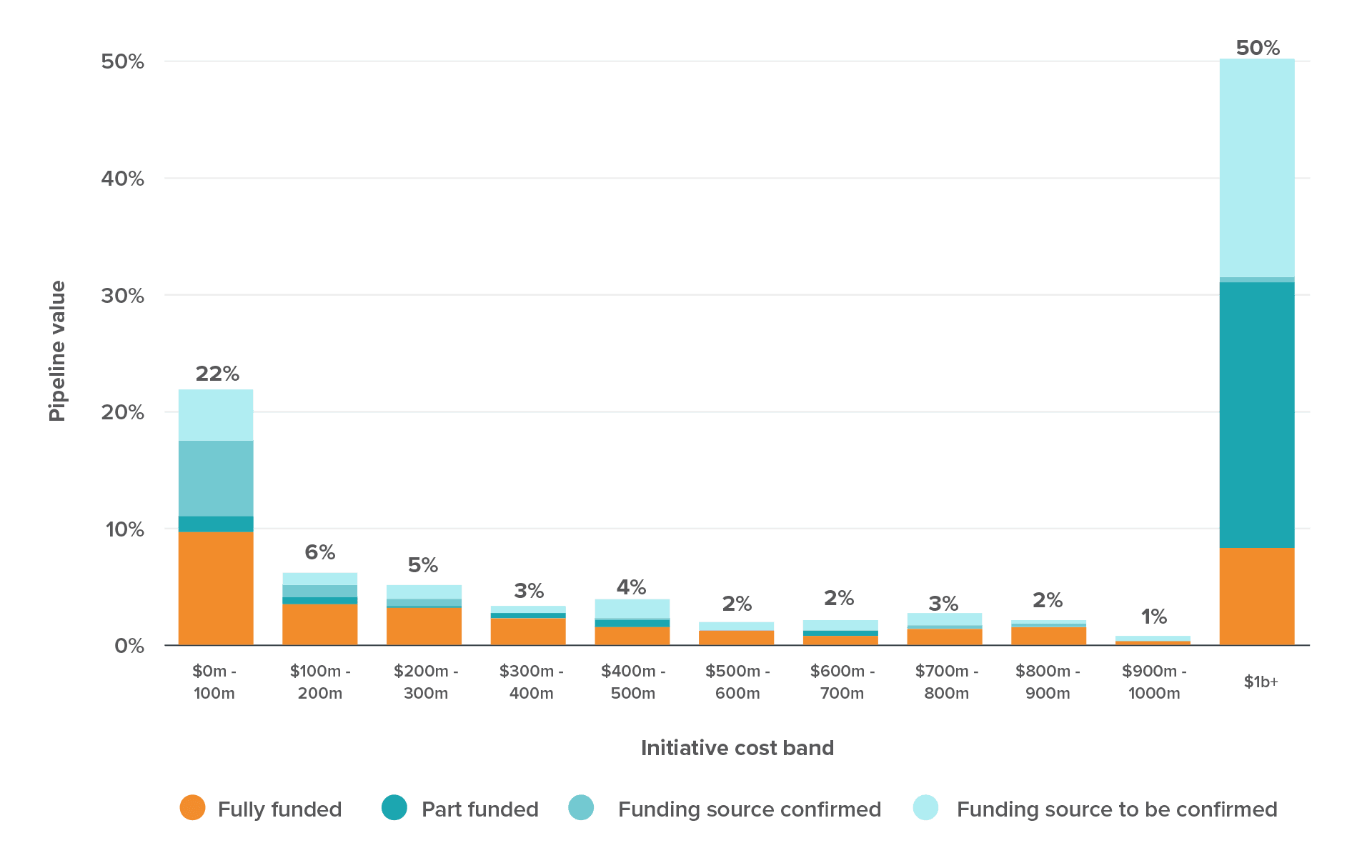

Figure 1 shows the distribution of Pipeline initiatives by cost band and funding status. The figure highlights that 22% of total Pipeline value comes from 12,109 initiatives (97% of all Pipeline initiatives), with expected costs of below $100 million. Of these, 4,817 initiatives (39% of all Pipeline initiatives) have expected costs of between $1 million and $25 million, and 6,655 initiatives (54%) have expected costs below $1 million.

Smaller initiatives make an important contribution to stability and confidence in the forward works programme. Of initiatives with an expected cost below $100 million, 72% have a confirmed funding source, representing 17% of total Pipeline value. Those that are fully funded represent a greater share of confirmed value than those initiatives over $1 billion.

These very large initiatives, with an expected cost exceeding $1 billion, number 46 and collectively account for 50% of total Pipeline value. Many remain in early stages and represent significant investment decisions for New Zealand:

- Twelve were reported as fully funded (8% of total Pipeline value)

- Eighteen were reported as part funded (23% of total Pipeline value)

- Fifteen were reported without a confirmed funding source (19% of total Pipeline value).

Figure 1: Together smaller initiatives have more funding certainty than very large projects

Distribution of initiatives in the Pipeline by expected initiative cost, March 2026

Funding commitments for initiatives

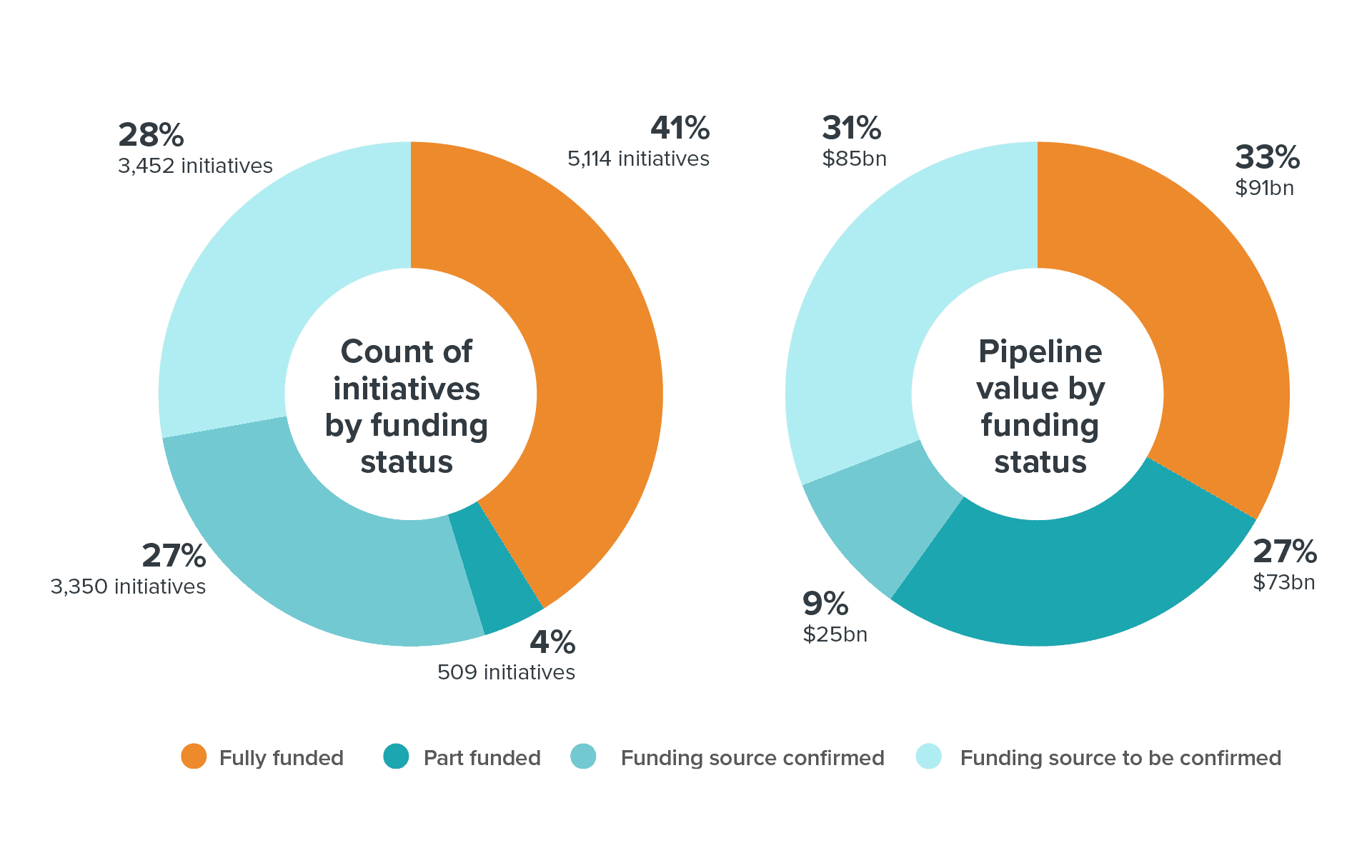

One-third of Pipeline value has full funding commitment

The view provided through the Pipeline of committed investments and unfunded investment options (or opportunity costs) is important to inform funding decisions. The Commission continues to work with contributors to improve the clarity in the reporting of funding status. Figures 1 and 2 illustrate the funding status breakdown for Pipeline initiatives.

Figure 2: $91 billion of Pipeline initiatives are fully funded

Pipeline value and initiative count by funding status, March 2026

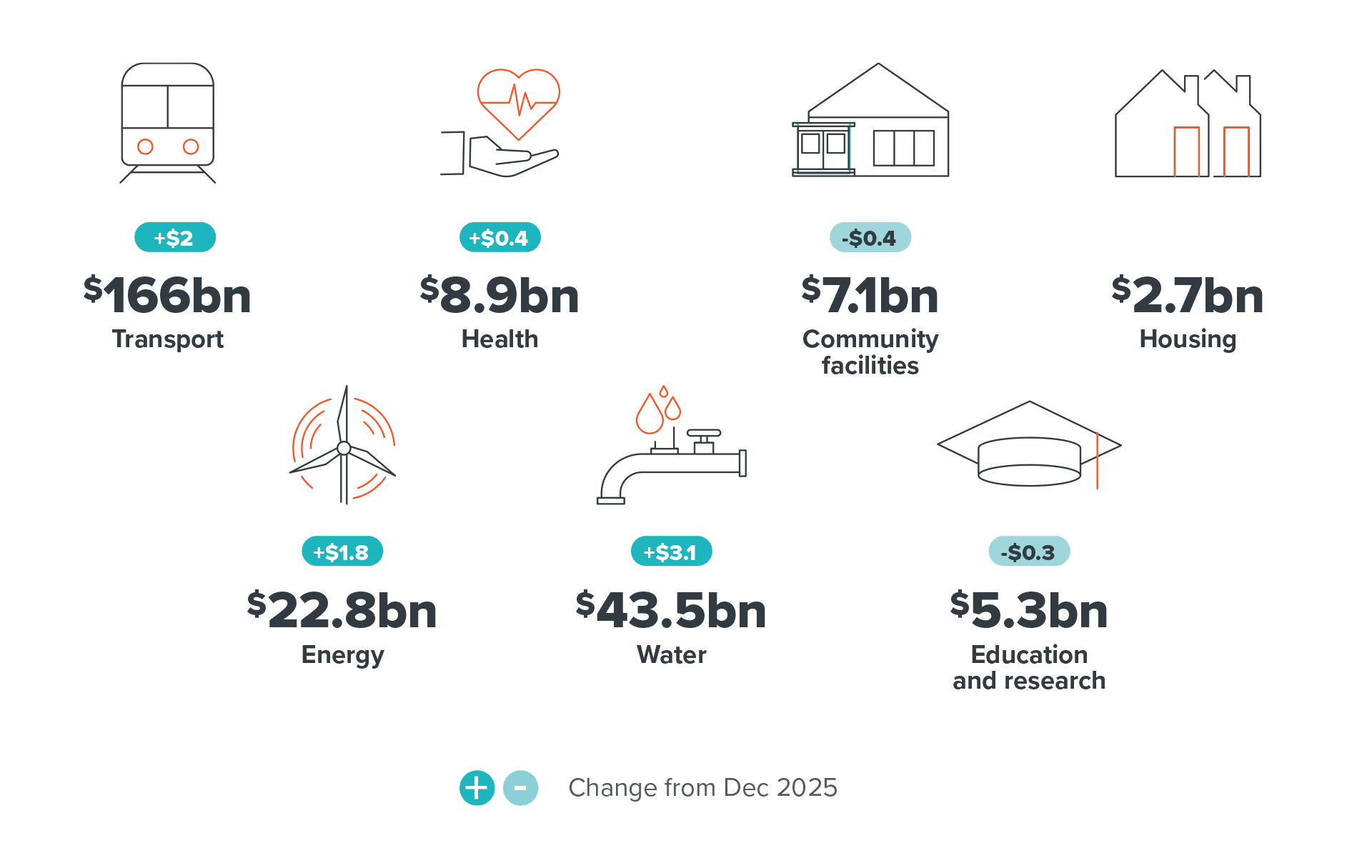

Investment across sectors

A sector view of the Pipeline shows where investment is weighted across New Zealand's infrastructure system, highlighting significant investment in transport infrastructure.

Activity in the construction market

How initiatives impact the construction market depends on many factors, including their value, funding commitment, scheduling, and planned speed of delivery. The Commission models both the spend and workforce demand signalled through the initiatives submitted to the Pipeline.

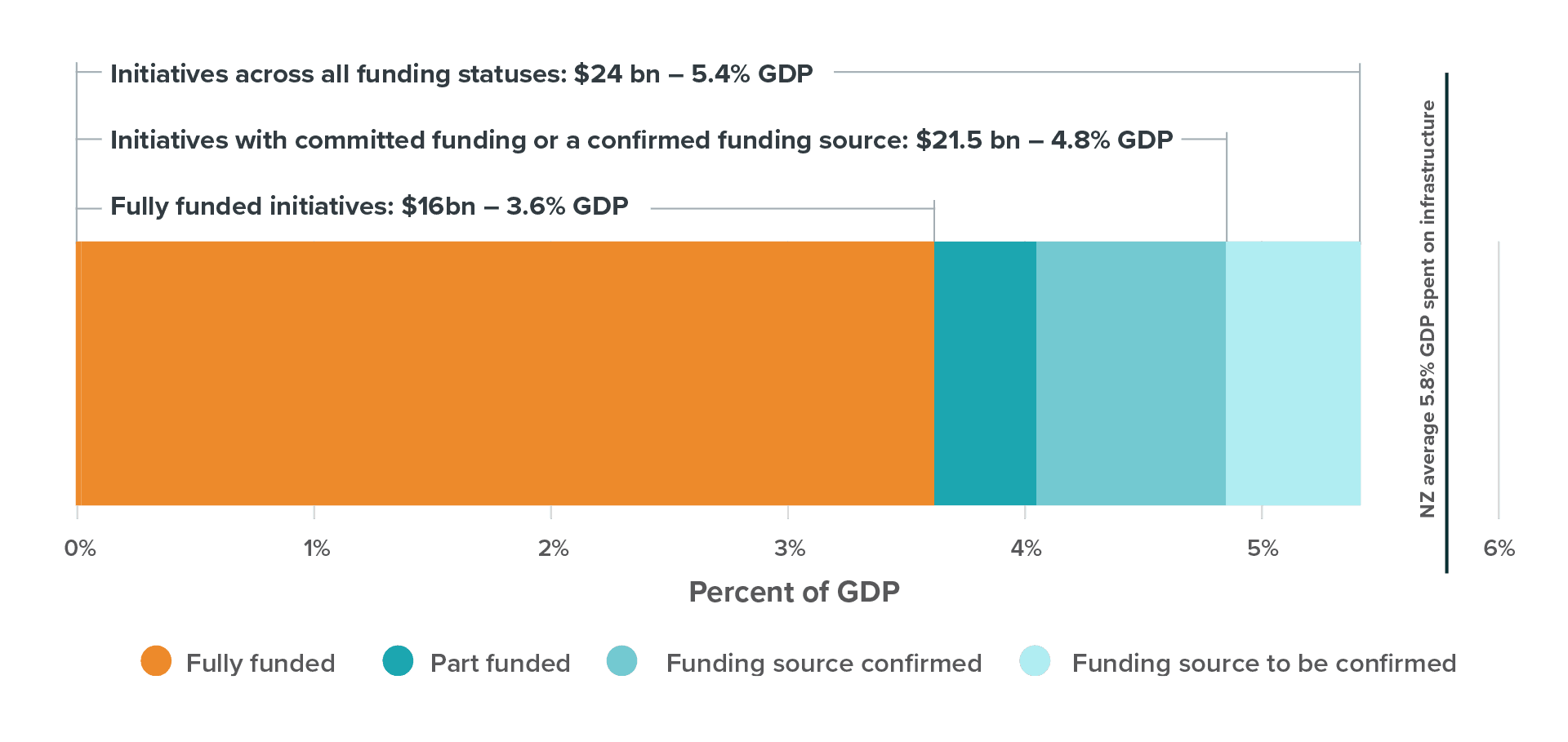

Pipeline commitment for 2026

The March 2026 Pipeline update indicates total projected spend of $21.5 billion in 2026 for initiatives with committed or confirmed funding sources. The Commission’s research indicates New Zealand has spent an average of 5.8% of GDP on infrastructure over the last 20 years.

The $21.5 billion projected spend 2 equates to approximately 4.8% of GDP, suggesting the Pipeline captures a significant proportion of near-term infrastructure activity. For fully funded initiatives alone, projected 2026 spend is $16 billion, or 3.6% of GDP.

Figure 3 illustrates how 2026 projected spend compares to the 5.8% historical GDP average. Of the $91.3 billion of initiatives that are fully funded, our modelling estimates approximately $48 billion of this will have been spent on these active projects.

Figure 3: 2026 spend for all initiatives in the Pipeline is nearing 20-year average spend for infrastructure

Projected spend by funding status for 2026 as a per cent of GDP

Looking further ahead at projected spending

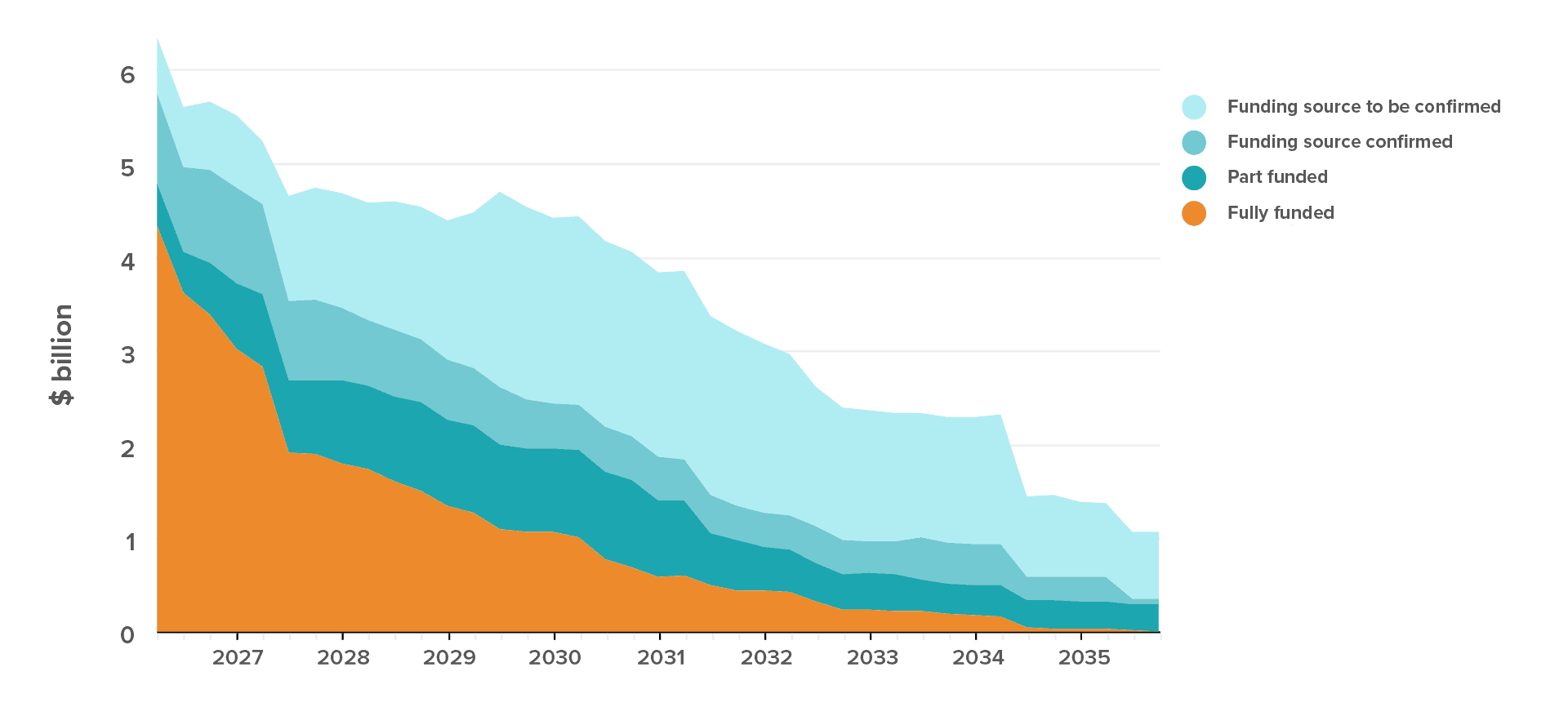

The projected spend for initiatives with confirmed funding sources for 2027 is currently $16.4 billion, increasing from $14.2 billion in December as project planning has progressed. Near-term projected spend figures generally rise each quarter as initiatives with short planning horizons are planned and submitted to the Pipeline, and as funding commitments progress.

As a measure of aggregate forward commitment, our projections indicate that three quarters of spend for initiatives with committed or confirmed funding sources will occur within 5 years – consistent with this forward measure from the previous quarter.

Building a stronger forward view – all funding statuses

The projected spend for initiatives currently

in planning and delivery is highlighted in the following figures:

- Figure 4: Projected spend by funding status, shows spend with the relative split of funding commitment over time. Large, committed initiatives drive spend further forward into the future, while the remainder of initiatives wait on investment decisions.

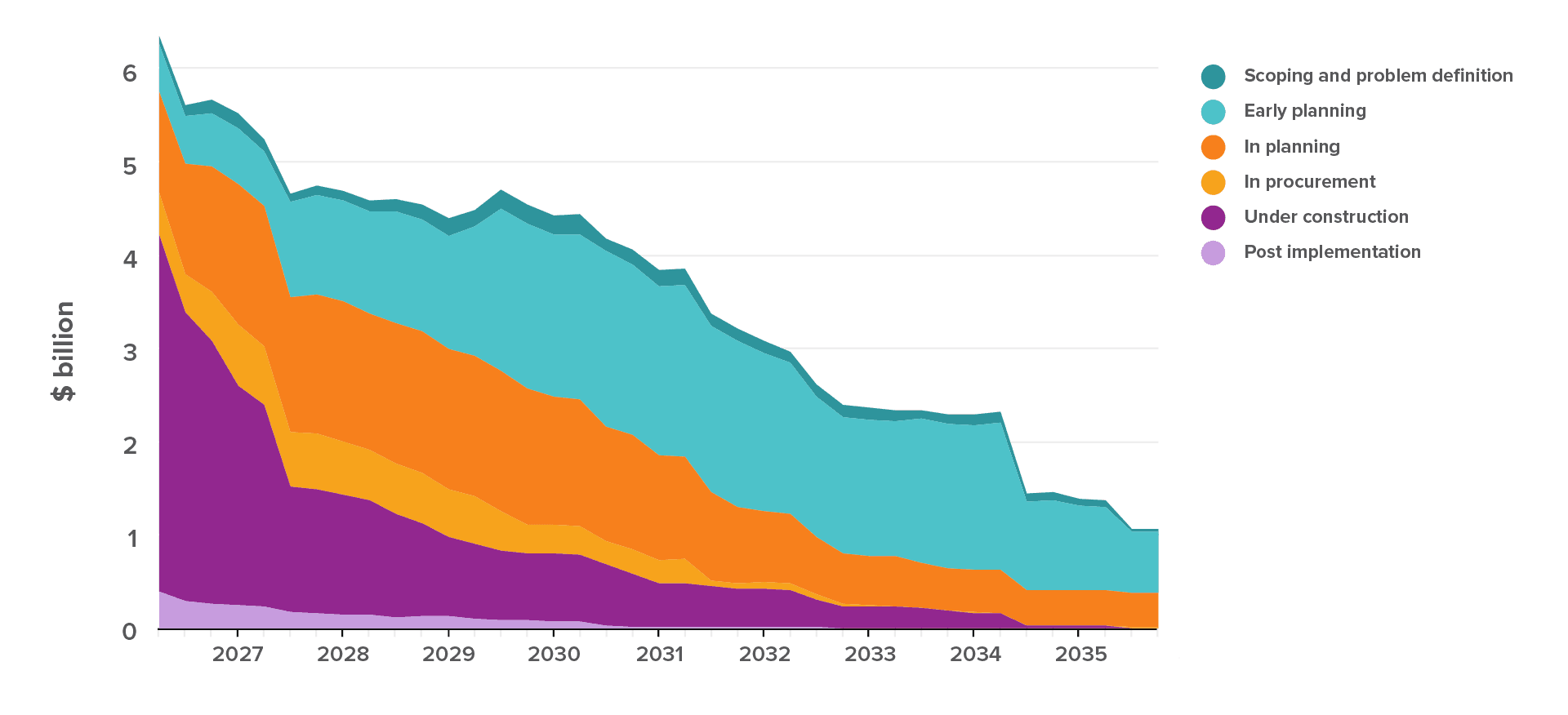

- Figure 5: Projected spend by initiative lifecycle status for all funding statuses shows a similar trend to Figure 4 and highlights the improving visibility of lower-certainty initiatives across the planning horizon.

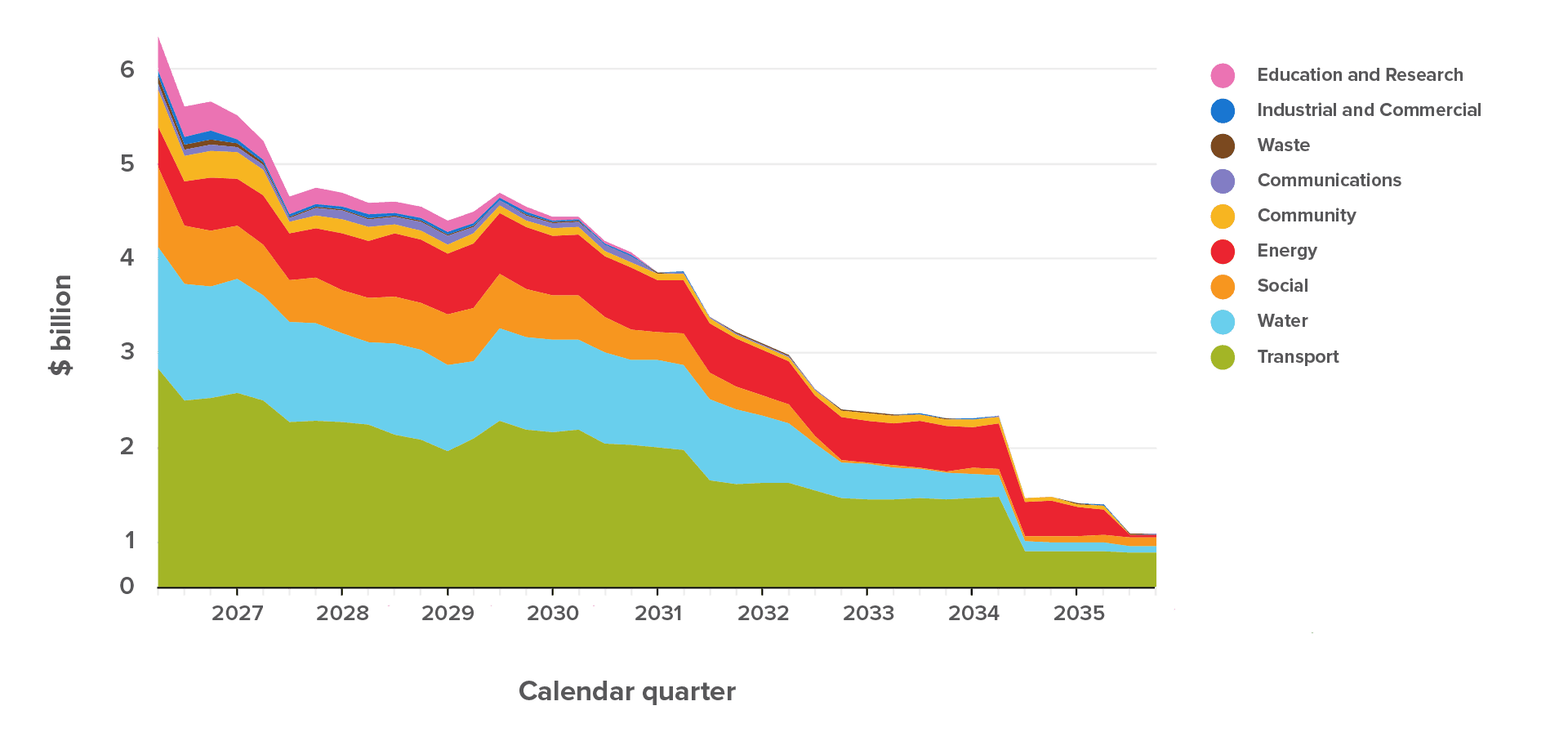

- Figure 6: Projected spend by sector highlights the scale of transport and water investment. Transport (including road, rail, ports, and airports) dominates projected infrastructure spend, accounting for $10.6 billion (44%) of total projected spend in 2026 and remaining above $7 billion annually through to 2031. Total projected transport spend from 2026 to 2036 is $72.8 billion, representing 50% of all-sector spend. Water is the second largest sector at$5 billion (21%) in 2026, with annual spend fluctuating between $1.3 billion and $5 billion through to 2033.

Figure 4: Almost two thirds of projected spend in the next ten years is funded or has a confirmed funding source

Projected quarterly spend by funding status, April 2026 – December 2035

Figure 5: Most unfunded spend comes from initiatives in early planning stages

Projected quarterly spend by initiative status, all funding statuses, April 2026 – December 2035

Figure 6: The transport and water sector account for more than 50% of projected spend over the next ten years

Projected quarterly spend by sector, all funding statuses, April 2026 – December 2035

Planning for workforce needed to deliver the Pipeline

An early view of workforce demand (and measures of certainty) relative to regional market capacity is important for planning, coordination, and scheduling of work. It helps training institutions, the construction sector, and regions to make informed decisions on investments in developing the skills and workforce that will be needed.

The infrastructure workforce is part of the wider construction workforce, much of which is dominated by housing construction activity. Around one third of the construction workforce is employed within the infrastructure sector.

Building a view of forward workforce demand – all funding statuses

The projected workforce demand 3 to deliver initiatives currently in planning and construction is highlighted in the following figures:

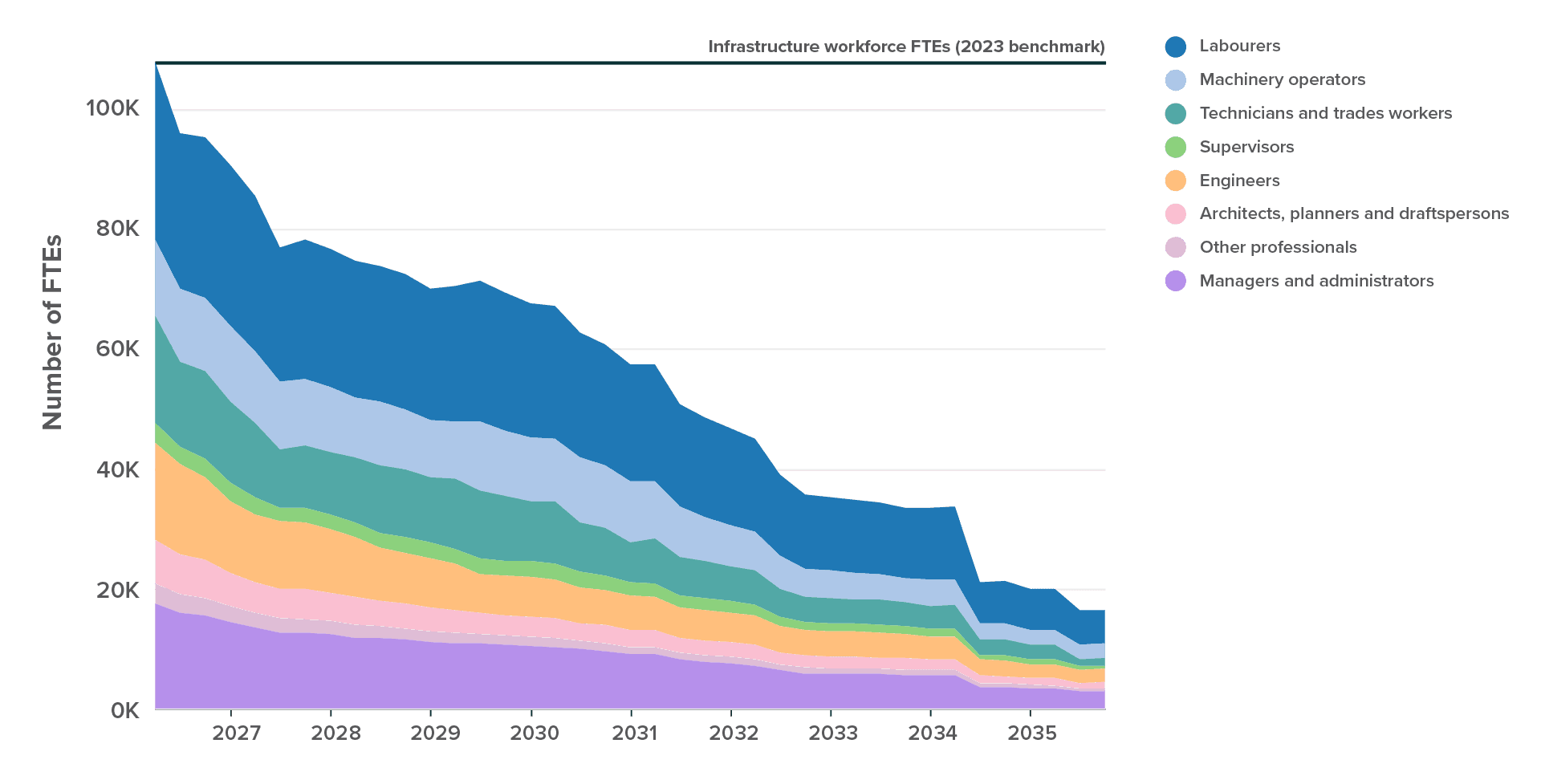

- Figure 7: Projected workforce demand by occupation group shows the full-time equivalent (FTE) workforce required to deliver Pipeline initiatives over the next 10 years, with a 2023 benchmark included as a reference point for where capacity may be available or delivery may become constrained.

- Figure 8: Projected workforce demand by construction timing illustrates how initiatives anticipated to enter construction in the near and medium term may influence workforce demand across the 10-year horizon.

Follow the chart links below to our insight platform and login to generate more insights for your region, sector or industry.

Figure 7: Projected workforce required to deliver initiatives in the Pipeline

Projected demand for workers (FTEs) each quarter, by occupation group (all funding status), April 2026 – December 2035

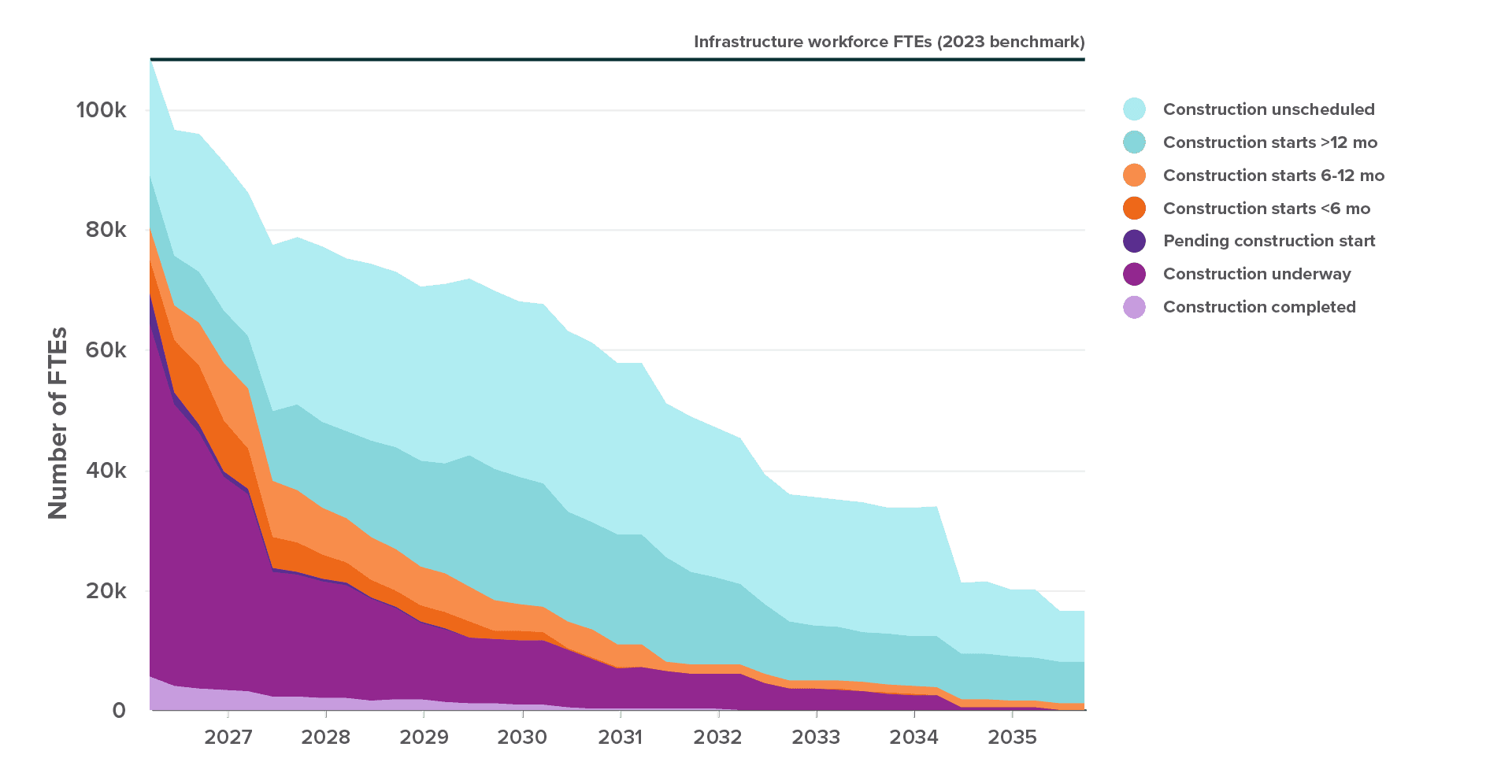

Figure 8: National workforce demand from initiatives scheduled to enter construction

Projected demand for workers (FTEs) each quarter, by construction start status (all funding status), April 2026 – December 2035

Unpacking the change in value between quarters

Fully funded initiatives increased by $5.5 billion

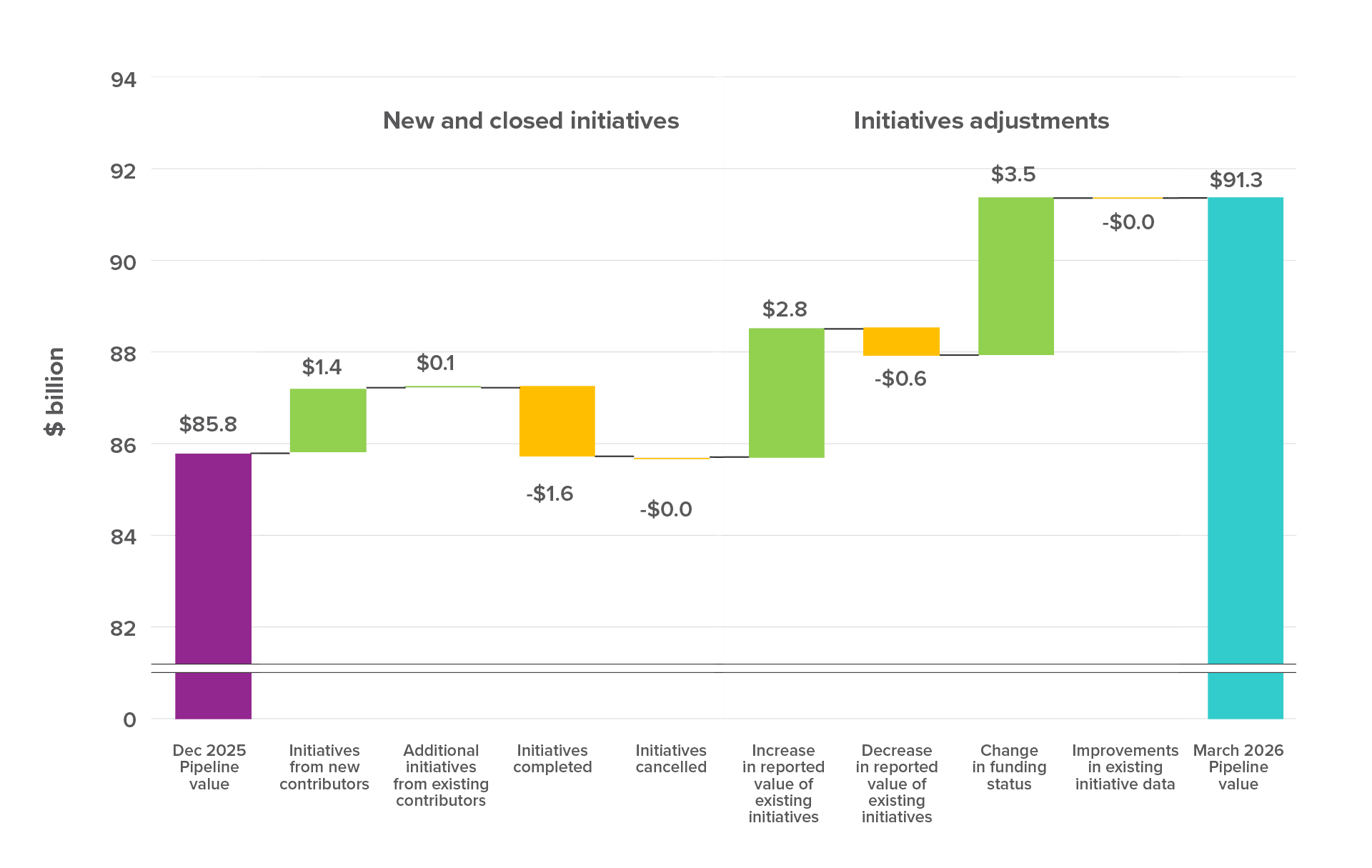

The net increase in the value of initiatives reported with full funding increased by $5.5 billion to reach $91.3 billion in March. The drivers of this change are highlighted in Figure 9 and included:

Increases in fully funded Pipeline value

- $4 billion of existing initiatives progressed to fully funded status.

- $1.5 billion of new fully funded initiatives were added to the Pipeline.

Decreases in fully funded Pipeline value

- $0.5 billion of initiatives moved from fully funded status to a lower-certainty funding status.

- Balancing the net changes were initiatives that were completed and those reported with a reduction in expected costs.

Figure 9: Fully funded value increased due to new initiatives added to the Pipeline, increases in expected initiative cost, and initiatives’ funding status progressing

Changes in Pipeline value for initiatives with confirmed funding sources, December 2025 – March 2026

Total value in the Pipeline increased by $6.7 billion

In terms of the total value of the Pipeline (inclusive of initiatives without confirmed sources, and regardless of initiatives’ progress through the project lifecycle) the net change was an increase of $6.7 billion from $267.7 billion to $274.4 billion in March. The drivers of this change are highlighted in Figure 10 and included:

Increases in total Pipeline value

- $5.7 billion of additional initiatives including:

- $3.1 billion provided by new organisations

- $2.6 billion from existing contributors

- $5.7 billion from adjustments to the expected cost of existing initiatives

Decreases in total Pipeline value

- $1.7 billion from initiatives completed during the quarter

- $0.2 billion from initiatives cancelled during the quarter

- $1.9 billion from adjustments to the expected cost of existing initiatives

- Quality adjustments resulted in a net decrease of $0.8 billion in Pipeline value

Figure 10: Introduction of new initiatives resulted in an increase to the overall value of the Pipeline

Changes in total Pipeline value including unfunded initiatives, December 2025 – March 2026

Diving deeper into the drivers of change

Adjustments to expected costs of initiatives

Adjustments to the expected costs are a significant contributor to changes in Pipeline value. In the current environment, fuel prices will be placing upwards pressure on costs of construction activity. We are observing cost increases in both planning and construction phases of projects, although improvements in how data is reported by contributors also account for some increases.

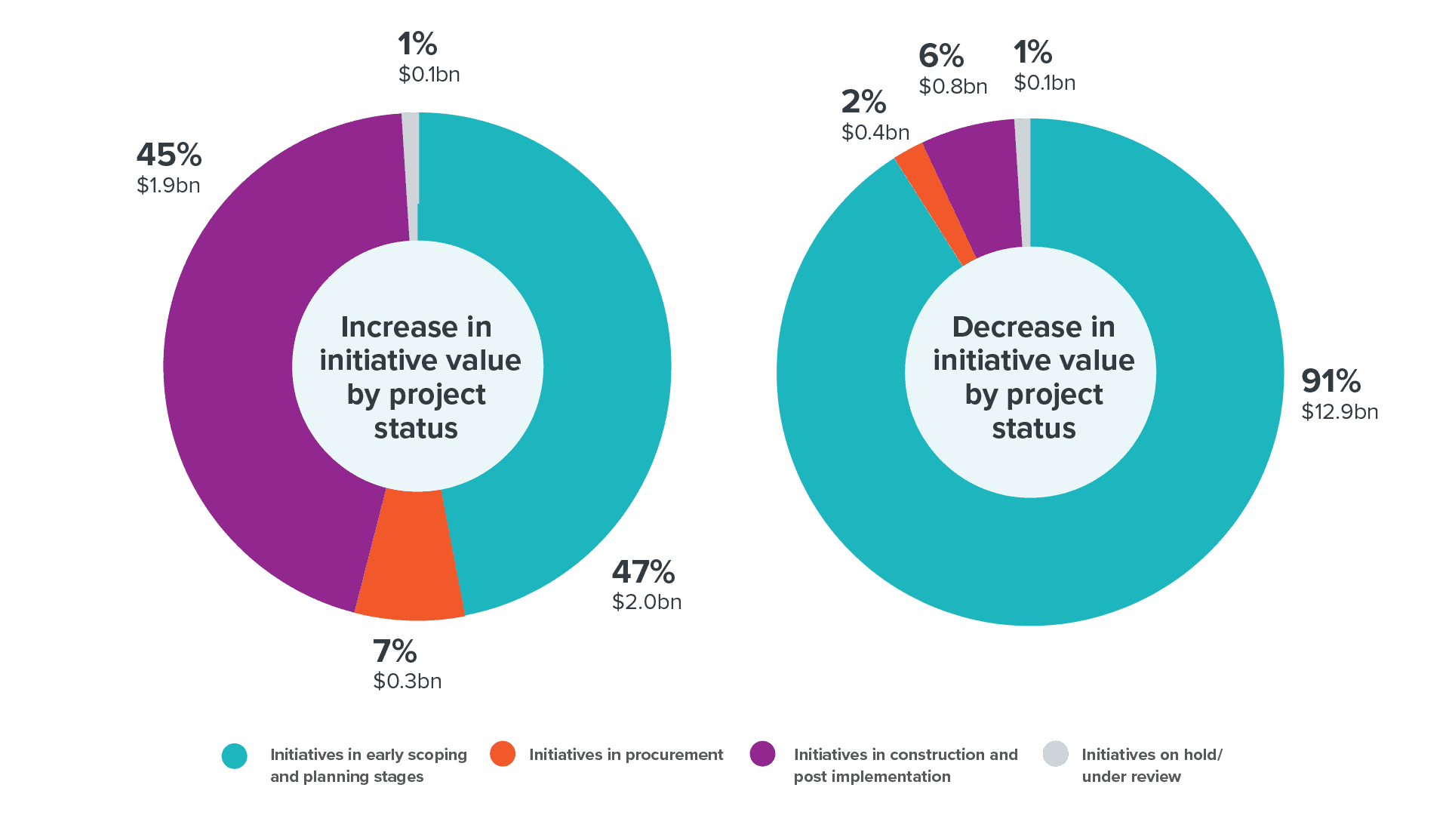

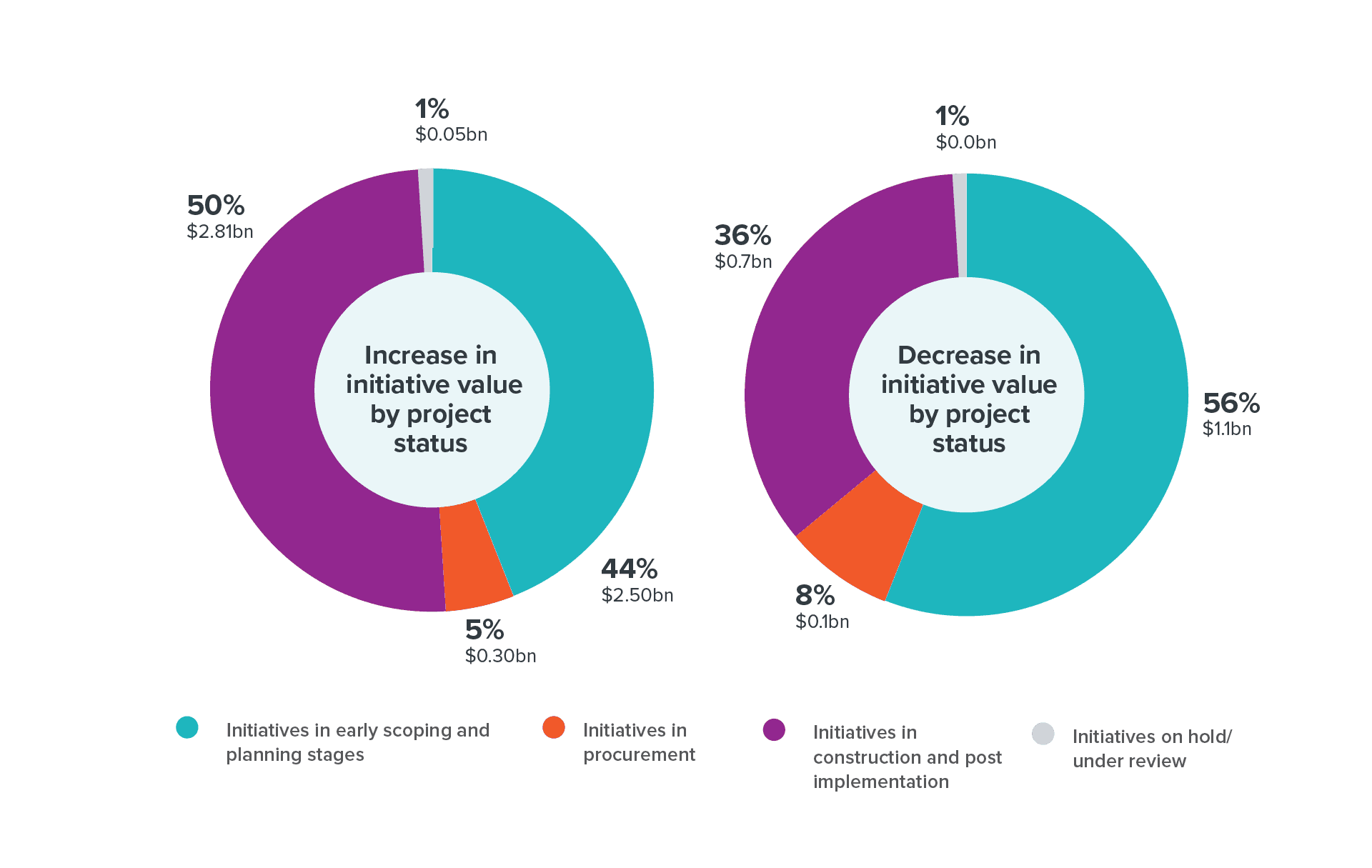

In early planning stages cost estimates typically carry a lower degree of confidence and are more readily revised as planning matures. Adjustments reported in March had a net result of adding $3.8 billion in Pipeline value. Drivers of change are highlighted in Figure 11 and included:

$5.7 billion increase in expected costs

- 44% came from 549 initiatives in early scoping and planning

-

50% came from 566 initiatives in construction or post implementation 4

-

$1.9 billion decrease in expected costs

-

56% came from 353 initiatives in early scoping and planning

-

36% came from 396 initiatives in construction or post implementation

-

Figure 11: March showed adjustments in initiative value across the project lifecycle

Lifecycle status for Pipeline initiatives that increased or decreased in reported value since December 2025

Infrastructure projects that have been delivered

As projects are completed, their value is removed from the Pipeline totals which are focused on current and future activity. Tracking projects through to completion forms our picture on how New Zealand delivers infrastructure.

In the March quarter, 400 initiatives worth $1.7 billion in total value, from 48 contributing organisations, were completed. Table 3 highlights selected projects completed during the quarter demonstrating the range of infrastructure being delivered across New Zealand and reported through the Pipeline.

Table 3: Initiatives reported as completed between December 2025 and March 2026

Towards a complete Pipeline

Created in 2020, the Pipeline continues to build towards a trusted and complete view of infrastructure planning, investment, and construction activity in New Zealand. Te Waihanga administers the Pipeline to fulfil our statutory functions to provide and coordinate information about infrastructure projects and promote a strategic and coordinated approach to delivery. 5

Pipeline contributors by organisation type and value

In total, 135 organisations now contribute to the Pipeline, an increase of 18% on twelve months ago, reflecting continued growth in organisational coverage. Grey District Council, Napier City Council, Oranga Tamariki – Ministry for Children, Southern Infrastructure, and Ministry of Business Innovation and Employment joined as new contributors in March, and 82% of contributors provided updates, adding new initiatives, making changes, or confirming their information remained correct.

Commercial Pipeline contributors include four State owned enterprises, two mixed ownership model electricity companies, four electrical lines companies covering 54% of the installation control points (ICPs) 6 and 75 councils (96% of councils across New Zealand).

Kawerau District Council, Mackenzie District Council, and Manawatu-Whanganui Regional Council are yet to contribute.

Make the most of the Pipeline

Join the programme and profile your projects

Organisations responsible for infrastructure that are not yet contributing to the Pipeline are encouraged to contact Te Waihanga to discuss participation. To add initiatives or ensure existing information is kept current, please get in touch.

Informing decisions for better infrastructure outcomes

The Pipeline forms an important evidence base to support a coordinated approach to infrastructure delivery across sectors, regions, and markets. Insights from the Pipeline enable understanding of investment options, opportunity costs, competing demand for construction resources and workforce, which highlights constraints or opportunities in the market.

The Pipeline helps inform policy development and the Commission’s advice on improvements to the wider infrastructure system, as well as Government demand-side decisions (such as increasing or curtailing demand through funding and other settings), and supply-side decisions (such as economic, education, and employment initiatives and settings).

Infrastructure providers use the forward view the Pipeline provides to inform prioritisation, coordination, planning, and investment decisions. Construction sector stakeholders use the Pipeline to understand upcoming business opportunities and the workforce capability

and capacity needed to deliver infrastructure. Regional economic development and employment agencies use the Pipeline to inform decisions on skills attraction, workforce planning, and regional investment timing.

View previous snapshots

Pipeline Snapshot: September - December 2025

Download

Pipeline Snapshot: July - September 2025

Download

Pipeline snapshot: April - June 2025

Download

Pipeline snapshot: January - March 2025

Download

Pipeline snapshot: October - December 2024

Download

Pipeline snapshot - July-September 2024

Download

Pipeline snapshot April - June 2024

Download

Pipeline Snapshot: January - March 2024

Download

Pipeline Snapshot: October - December 2023

Download

Pipeline snapshot: July - September 2023

Download

Pipeline snapshot: April - June 2023

Download

Pipeline snapshot: January - March 2023

Download

Pipeline snapshot: October - December 2022

Download

Infrastructure Quarterly - November 2022

Download

Infrastructure Quarterly - August 2022

Download

Infrastructure Quarterly - January 2022

Download

Infrastructure Quarterly - May 2022

Download

Infrastructure Quarterly - October 2021

Download

Infrastructure Quarterly - July 2021

Download

1 The Pipeline programme includes initiatives provided in confidence. These initiatives inform aggregate totals and projected spend and workforce demand, but

are not released at record level.

2 Spending modelling is based on reported value and timing of initiatives in the Pipeline. Actual timing of project spend may differ from projections. March 2026

includes an update to the Commission’s spend model to enhance the modelling and improve the alignment with our workforce modelling. These changes have

resulted in some differences to the previous modelling approach.

3 Workforce demand modelling is based on reported value and timing of initiatives in the Pipeline. Actual workforce demands may differ from projections. The

projections may overstate near-term demand (where initiatives are unfunded or at an early stage) or understate it (where the Pipeline does not yet cover all

infrastructure activity), both factors should be considered when interpreting these figures.

4 Movements in expected initiative costs can be driven by improved reporting practices that better reflect the full potential cost of an initiative, rather than by changes in scope or cost escalation. Our goal is to improve reporting practices to provide more confidence in these statistics.

5 New Zealand Infrastructure Commission/Te Waihanga Act 2019 (https://www.legislation.govt.nz/act/public/2019/51/en/latest/#LMS155571)

6 An ICP is an installation control point or the point of connection to an electricity network where an electricity retailer is deemed to supply electricity to a consumer.